What is gearing?

What is gearing?

Put simply, gearing is borrowing money to invest with the aim of magnifying, or ‘gearing’, returns. It is important to highlight that gearing investments magnifies losses, as well as gains.

One of the most common forms of geared investments is a mortgage on an investment property. The same principle applies to gearing shares; money is borrowed to invest and the shares are used to secure the loan, just as the property is used to secure a mortgage.

Margin lending and professionally-managed geared funds are two of the most common ways of implementing a gearing strategy in the sharemarket.

How does gearing work?

The key principle behind gearing is quite simple; the investment made with borrowed money is expected to rise by more than it costs to borrow the money.

Let’s say an investor has $10,000 to invest. Over the course of the year their investment rises by 10%. This means their investment is now worth $11,000; a difference of $1,000

To illustrate how borrowing money can magnify returns, let’s say the same investor has $10,000, but this time borrows an additional $30,000, making a total of $40,000 to invest. The investment also rises 10%. This means their investment is now worth $44,000; a difference of $4,000.

While the magnification of returns is plain to see, it’s important to remember that the investment must rise more than the cost of borrowing. In this example, if the interest rate on the loan is 10% pa, the net return is the same as for an ungeared investment.

A geared fund therefore will not always magnify market gains. This is particularly the case in a low-return or high borrowing-cost environment.

As previously mentioned, gearing can magnify losses as well as gains.

This time let’s say the investment falls 10% in value. A $10,000 investment will be worth $9,000; a difference of -$1,000, while a $40,000 investment will be worth $36,000; a difference of -$4,000.

However, again it is again important to remember the cost of borrowing. If the interest rate on the $30,000 loan is 10% pa, that’s an additional $3,000 in costs; a total difference of -$7000.

These examples illustrate that while gearing may not always magnify gains, it will always magnify losses.

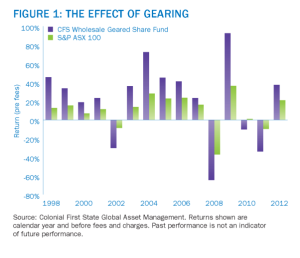

The effect gearing has on returns and the increased volatility is illustrated in Figure 1, which compares the calendar year returns of the Colonial First State Wholesale Geared Share Fund to its benchmark, the S&P ASX 100.

Gearing concepts explained Loan to value ratio

The loan to value ratio (LVR), sometimes known as the gearing ratio, is the amount of gearing undertaken. The higher the LVR, the more risky the strategy becomes.

If an investor has $10,000 to invest and borrows an additional $10,000, the LVR is 50%. This is calculated because the $10,000 borrowed is 50% of the total investment ($20,000).

To securitise a margin loan, lenders will set a maximum LVR, usually around 75%. On a $10,000 loan this would involve borrowing $30,000 to make a $40,000 total investment (a $30,000 loan is 75% of a $40,000 investment).

Margin calls

If an investor takes out a margin loan to invest directly in shares, they are subject to the possibility of a margin call.

A lender can make a margin call if the LVR rises above a certain threshold. Using the example above, if the value of a $40,000 investment drops 10% to $36,000 the LVR becomes 83%.

One of two things must happen when a margin call is made:

• the borrower must make a payment into the loan to bring the LVR back within the threshold or

• the borrower must sell shares; the proceeds of which will go to repay the loan to bring it back within the LVR threshold. This has the undesired effect of crystallising losses in an investment portfolio.

Gearing strategies

Gearing in equity markets can be obtained by taking out a margin (or similar) loan to invest directly in shares, or through a professionally-managed geared fund. There are important differences between the two strategies.

Gearing within a managed fund

The manager of an internally geared fund arranges the borrowing within the fund. This means investors gain access to leveraged market exposure without being personally liable for the fund’s borrowings. There is no personal obligation to repay the debt, as the debt is incurred by the fund as an institutional borrower, rather than by an individual.

Large institutional borrowers can often access cheaper loan rates than are available to individuals. This typically results in a lower borrowing costs compared with other forms of borrowing, such as margin lending. However, there are fees and charges associated with investing in a managed fund which you need to consider Details of fees and charges are available in any fund’s Product Disclosure Statement.

The LVR is usually actively managed by a fund. Therefore investors don’t receive margin calls forcing them to take action, as can occur with margin lending. Most funds will actively monitor gearing levels to ensure they remain within a desired range.

Internally geared funds comply with the superannuation borrowing rules, and are generally permissible investments for superannuation. As many superannuation investors have many years, or even decades, until retirement, investments with long-term horizons, such as internally geared funds, may be a suitable part of an investment portfolio.

Internally managed geared funds are managed by investment professionals who will actively manage the investment decisions and gearing process. This reduces the paperwork and effort which is often involved in other forms of geared investments.

An internally managed geared fund will usually have broad diversification over many companies and sectors. This has the effect of lessening the impact of any individual stock’s or sector’s performance on the overall portfolio. The level of diversification in a managed fund can be difficult to replicate efficiently by individual investors.

Summary

Geared funds are not for everyone, and investors should ensure that they are comfortable with risks associated with geared funds and the potentially large fluctuations, both up and down, in the value of their investment. Investors should also consider an investment outlook of at least seven years. Because of the high risks involved with gearing, it is important to speak with a financial adviser before making an investment decisions.

Financial Planning is about much more than retirement

/in Financial Advice General Info, Investment Financial Advice /by Fil-BattistiIf you are interested in investing, there are several things you need to consider. For example, how long do you have to invest and how comfortable are you with fluctuations in the value of your investments? We can help you determine your time horizon and risk profile and then recommend the most suitable type of investments to help you realise your goals.

What about your super? Is it working as hard as you are? Your risk profile can also be applied to your superannuation investments. It’s a long-term investment, but it’s important to make sure it’s invested in the right way.

Limits to the amount of super you can contribute each year ($25,000 in concessional contributions for people under 60 and $35,000 for those aged 60 and over) means the earlier you start, the better. Contributing more to super will not only boost your super balance, it could even reduce the amount of tax you pay!

Everybody’s different – different needs, different goals and different circumstances, however, professional financial advice can help you at every stage of your life.

We can provide guidance on:

To start planning for a successful financial future, call us today to make an appointment.

Source I IOOF

The Importance of Trauma Cover

/in Personal Risk Financial Advice /by Fil-BattistiOur new case study will help you understand the importance of trauma cover when facing serious illness.

One in two Australians will develop cancer before the age of 85 and one in five will die from the disease, according to a report from the Australian Institute of Health and Welfare (AIHW).

But while the incidence of all cancers rose by 27 per cent in the 25 years to 2007, deaths from the disease have actually fallen by 16 per cent. This proves just how far modern medicine has come and the calibre of treatments available to treat the various forms of this illness.

In fact, this report has revealed that cancer patients are increasingly living longer with 66 per cent now surviving for at least five years (for all cancers combined in the period 2006-2010) – a large increase from the 47 per cent survival rate for all cancers in the period 1982-1987.

According to Anne Bech, spokeswoman for AIHW, “While overall cancer survival is improving in Australia variations still exist between types of cancer.”

The report also revealed that cancer sufferers, who have survived for five years, had a 90 per cent chance of living for another five years for all cancers combined. This is all good news right? Well if you have enough money to cover all the necessary (and ongoing) treatments then absolutely! But what if you can’t afford to be treated?

One might be forgiven for thinking that a combination of income protection insurance, private health insurance and Medicare are enough to cover the treatment of serious illness. But the truth is, in the case of cancer, where it can take years of treatment including many rounds of chemotherapy, radiotherapy and even surgery, serious illness can come at a huge cost which can mean hundreds of thousands of dollars out of your pocket.

It’s important to speak to us to understand the difference a lump sum payment can make in the event of suffering a pre-defined traumatic event such as cancer.

Not only will trauma cover help to meet any out of pocket expense you might face, but it could in fact, ultimately assist with the road to recovery by removing some of the added financial pressure created by the need for ongoing and often expensive treatments.

Are you financially prepared for the treatments that go along with surviving serious illness?

For more information on trauma cover to put your mind at ease, contact us today.

Source I Zurich

Understanding Geared Investments

/in Financial Advice General Info /by Fil-BattistiPut simply, gearing is borrowing money to invest with the aim of magnifying, or ‘gearing’, returns. It is important to highlight that gearing investments magnifies losses, as well as gains.

One of the most common forms of geared investments is a mortgage on an investment property. The same principle applies to gearing shares; money is borrowed to invest and the shares are used to secure the loan, just as the property is used to secure a mortgage.

Margin lending and professionally-managed geared funds are two of the most common ways of implementing a gearing strategy in the sharemarket.

How does gearing work?

The key principle behind gearing is quite simple; the investment made with borrowed money is expected to rise by more than it costs to borrow the money.

Let’s say an investor has $10,000 to invest. Over the course of the year their investment rises by 10%. This means their investment is now worth $11,000; a difference of $1,000

To illustrate how borrowing money can magnify returns, let’s say the same investor has $10,000, but this time borrows an additional $30,000, making a total of $40,000 to invest. The investment also rises 10%. This means their investment is now worth $44,000; a difference of $4,000.

While the magnification of returns is plain to see, it’s important to remember that the investment must rise more than the cost of borrowing. In this example, if the interest rate on the loan is 10% pa, the net return is the same as for an ungeared investment.

A geared fund therefore will not always magnify market gains. This is particularly the case in a low-return or high borrowing-cost environment.

As previously mentioned, gearing can magnify losses as well as gains.

This time let’s say the investment falls 10% in value. A $10,000 investment will be worth $9,000; a difference of -$1,000, while a $40,000 investment will be worth $36,000; a difference of -$4,000.

However, again it is again important to remember the cost of borrowing. If the interest rate on the $30,000 loan is 10% pa, that’s an additional $3,000 in costs; a total difference of -$7000.

These examples illustrate that while gearing may not always magnify gains, it will always magnify losses.

The effect gearing has on returns and the increased volatility is illustrated in Figure 1, which compares the calendar year returns of the Colonial First State Wholesale Geared Share Fund to its benchmark, the S&P ASX 100.

Gearing concepts explained Loan to value ratio

The loan to value ratio (LVR), sometimes known as the gearing ratio, is the amount of gearing undertaken. The higher the LVR, the more risky the strategy becomes.

If an investor has $10,000 to invest and borrows an additional $10,000, the LVR is 50%. This is calculated because the $10,000 borrowed is 50% of the total investment ($20,000).

To securitise a margin loan, lenders will set a maximum LVR, usually around 75%. On a $10,000 loan this would involve borrowing $30,000 to make a $40,000 total investment (a $30,000 loan is 75% of a $40,000 investment).

Margin calls

If an investor takes out a margin loan to invest directly in shares, they are subject to the possibility of a margin call.

A lender can make a margin call if the LVR rises above a certain threshold. Using the example above, if the value of a $40,000 investment drops 10% to $36,000 the LVR becomes 83%.

One of two things must happen when a margin call is made:

• the borrower must make a payment into the loan to bring the LVR back within the threshold or

• the borrower must sell shares; the proceeds of which will go to repay the loan to bring it back within the LVR threshold. This has the undesired effect of crystallising losses in an investment portfolio.

Gearing strategies

Gearing in equity markets can be obtained by taking out a margin (or similar) loan to invest directly in shares, or through a professionally-managed geared fund. There are important differences between the two strategies.

Gearing within a managed fund

The manager of an internally geared fund arranges the borrowing within the fund. This means investors gain access to leveraged market exposure without being personally liable for the fund’s borrowings. There is no personal obligation to repay the debt, as the debt is incurred by the fund as an institutional borrower, rather than by an individual.

Large institutional borrowers can often access cheaper loan rates than are available to individuals. This typically results in a lower borrowing costs compared with other forms of borrowing, such as margin lending. However, there are fees and charges associated with investing in a managed fund which you need to consider Details of fees and charges are available in any fund’s Product Disclosure Statement.

The LVR is usually actively managed by a fund. Therefore investors don’t receive margin calls forcing them to take action, as can occur with margin lending. Most funds will actively monitor gearing levels to ensure they remain within a desired range.

Internally geared funds comply with the superannuation borrowing rules, and are generally permissible investments for superannuation. As many superannuation investors have many years, or even decades, until retirement, investments with long-term horizons, such as internally geared funds, may be a suitable part of an investment portfolio.

Internally managed geared funds are managed by investment professionals who will actively manage the investment decisions and gearing process. This reduces the paperwork and effort which is often involved in other forms of geared investments.

An internally managed geared fund will usually have broad diversification over many companies and sectors. This has the effect of lessening the impact of any individual stock’s or sector’s performance on the overall portfolio. The level of diversification in a managed fund can be difficult to replicate efficiently by individual investors.

Summary

Geared funds are not for everyone, and investors should ensure that they are comfortable with risks associated with geared funds and the potentially large fluctuations, both up and down, in the value of their investment. Investors should also consider an investment outlook of at least seven years. Because of the high risks involved with gearing, it is important to speak with a financial adviser before making an investment decisions.

Second Marriage?

/in Financial Advice General Info /by Fil-BattistiGetting married, even if it’s for the second time, is a happy time but it does present some financial planning challenges.

Second marriages present some complex and contentious estate planning challenges.

While many partners in a second marriage want ‘their’ estate to be passed on to their own rather than their partner’s children, most do not take steps to ensure that happens. As a result, adult children from the first marriage often feel threatened by the second marriage and this can be a common source of disputes.

Feeling that their ‘rightful’ inheritance from their natural parent will be taken away from them and given to their step brothers and sisters often results in real tension between rival siblings both before and after death.

A vital first step to ensuring that assets are appropriately distributed is to have a Will in place. But it’s important to remember that marriage revokes any existing Will. So there is a real need to review your Will if you remarry.

The following are some of the issues you may need to address when making a Will:

Setting up a family trust is one way to isolate assets from the estate and potentially avoid these pitfalls.

Establishing a Testamentary Trust within the Will can also provide you with some flexibility as to how to deal with assets to provide for both a partner and children from your first marriage.

For more information on how to make sure your assets are distributed according to your wishes and your family’s and children’s futures are protected, speak to your financial adviser or a specialist estate planner.

Source | IOOF

1 Australian Bureau of Statistics, Disability, Ageing and Carers: Summary of Findings, 2003

This communication has been prepared on a general advice basis only. The information has not been prepared to take into account your specific objectives, needs and financial situation. The information may not be appropriate to your individual needs and you should seek advice from your financial adviser before making any investment decisions.

Investing for the Long Term

/in Financial Advice General Info, Investment Financial Advice /by Fil-BattistiInvesting over the long term can help you weather market fluctuation and make the most of compound returns.

It’s never too early to start investing. Whether the amount is small or large, the earlier you invest, the more likely you are of achieving a greater end result.

Market cycles

Investment markets tend to move in cycles. They can vary from providing strong returns year after year, known as bull markets, to bear markets where stock markets are declining.

It’s important to recognise that investing is generally for the medium (3-5 years) to long-term (5+ years) and understand there will be periods of both out performance and underperformance. Those with shorter time horizons and lower acceptance of risk often opt for more defensive asset types that are less prone to market movement, such as cash and fixed interest.

While defensive assets may provide greater shelter from volatility, they generally provide lower longer term returns than the other asset classes such as property and shares. This may result in you not achieving all of your financial goals and objectives.

Time in the market

It can be tempting to react to market volatility by jumping in and out of certain investments. But timing the market requires you to make two correct decisions that are very difficult to make: exactly when to buy and exactly when to sell. Being out of the market at the wrong time, even if it’s for a short period can significantly reduce the overall performance of your investments.

Markets will always fluctuate but the longer you stay invested, the less affected you are by short-term volatility.

The power of compound returns

The power of compounding returns is the single most important reason for you to invest early. The interest your account earns on your original investment increases your account balance and ongoing investment earnings can be made on both your original investment and the interest your account has returned. In other words, you receive interest on interest. When your assets compound for a long period of time, this can give a substantial boost to your investment.

Asset performance over the long term

For example, if you decide today to invest an initial amount of $1,000 into a managed fund that earns 8% p. a. and then contribute $100 per month, in 10 years’ time, you would have $20,071. If you started investing the same amount three years later, you would only have $12,708. This is where the power of compound returns takes effect. Spending more time in the market, or investing earlier, can make a big difference to your overall investment returns.

Benefits of dollar cost averaging

Dollar cost averaging (DCA) is a strategy of investing a fixed amount at regular intervals. DCA lowers the risk of investing a large amount into a single investment at the wrong time. The benefit of DCA is that the timing risk is reduced and as a result the cost is averaged out over time.

Within managed funds, for example, unit prices can fluctuate in response to market movements. By making regular investments rather than a one-off contribution, the unit price evens out over time.

When followed strictly, this strategy can help you reduce risk and avoid costly emotional and spontaneous investment decisions that might see you selling at the bottom of the market and buying in at the top.

Source I One Path